Offering payment terms is a core part of selling in B2B. It also turns vendors into lenders, but without the data and tools that banks use.

Banks are well-equipped to make credit decisions, as they have used machine learning to forecast default for decades. Yet most vendors still rely on aging reports and gut feel.

That's why we're launching Risk of Default Scores: a way to see the probability of default for each customer, right inside Wholesail's platform.

What’s new: a buyer-level probability of default

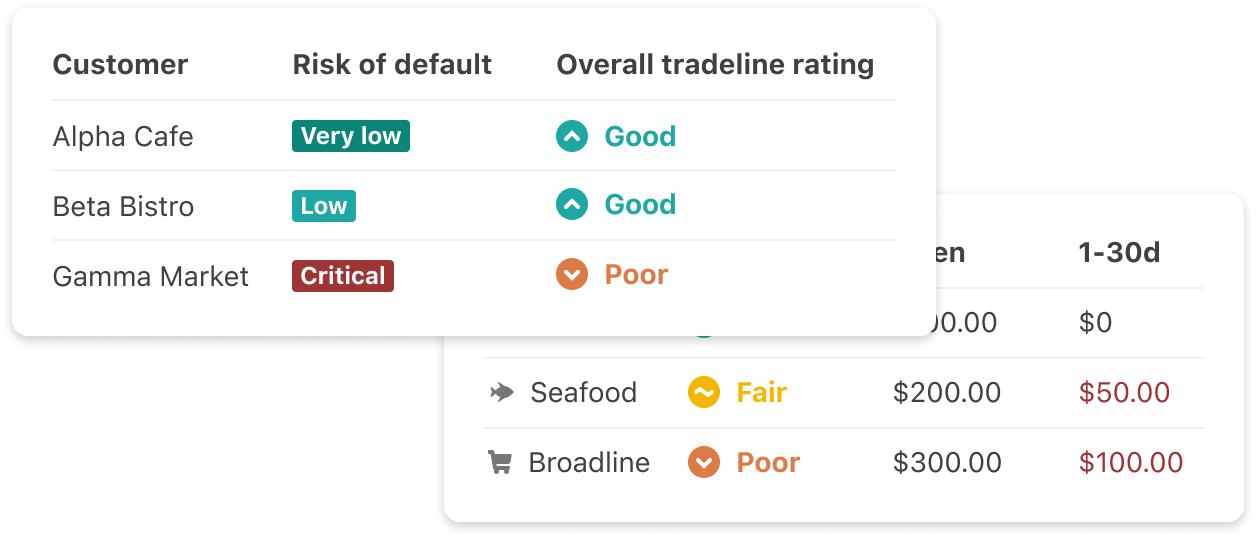

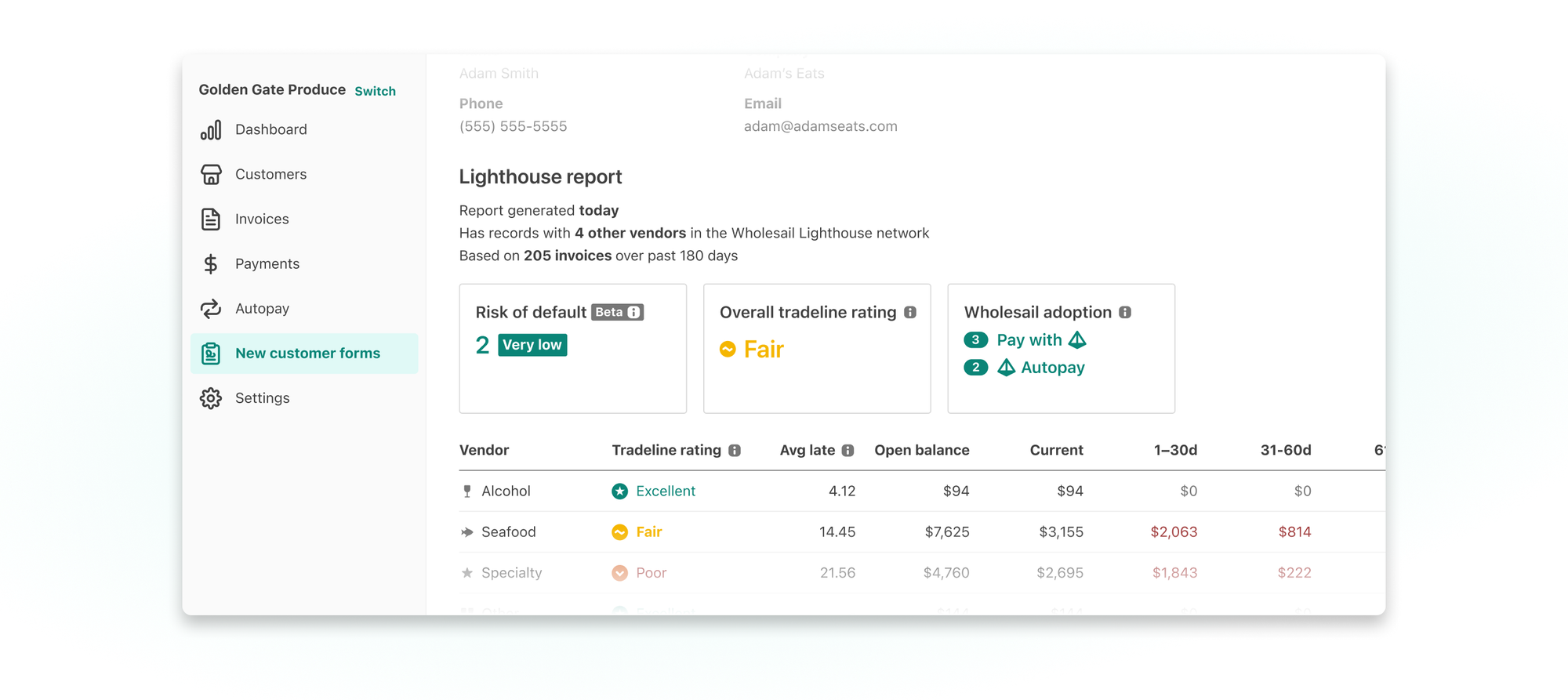

The Risk of Default score shows the likelihood that a buyer will default, and is grouped into 5 risk levels from 🟢 Very low to 🔴 Critical.

Once opted in to Lighthouse, the Risk of Default score is available for all existing customers with payment history, regardless of whether there's sufficient data for a full Lighthouse report with tradelines. For New Customer Forms, the score appears where there's sufficient Lighthouse network data.

Learn more about Lighthouse here: Extend credit terms with confidence

Why we built this

Collections and credit decisions typically rely on a few blunt tools:

- Past-due aging (how late someone is paying you)

- Incomplete credit bureau signals not built for wholesale trade credit

- Manual judgment calls prone to vary by team member, skill level, and bandwidth

The problem is that aging alone doesn't tell you who's actually headed toward default. A buyer can be only a week past due and still be on a path toward non-payment. Another buyer might consistently pay slow and never default. When you treat both the same, you waste time on the wrong accounts, and miss the ones that need attention.

But there's another side to this. In a recent Wholesail survey of 10,000 food and beverage buyers, 81% said short credit terms have led them to restrict their buying — and 60% said they'd order more if offered longer terms. That means overly conservative terms leave revenue on the table. The challenge has always been knowing which customers deserve longer terms, and which ones don't.

Risk of Default scores help you:

- Reduce losses by catching early warning signs before an account becomes a write-off, and prioritizing collections based on probability of non-payment rather than just days past due.

- Grow revenue by identifying which customers are genuinely low-risk, so you can extend better terms with confidence — terms that encourage larger orders and strengthen the relationship.

What the model learns from

Default is rarely caused by one factor. It's usually a combination of related factors across multiple vendor relationships.

A few of the signals we've found especially predictive:

- 🔺 Rising balances across vendors over time. One of the strongest indicators is when a buyer's balance keeps increasing across multiple vendors. That can reflect growing demand, or a sign of stretching payables to cover cash flow gaps. The difference is in the pattern over time.

- 🔺 Increasing days-late behavior. A buyer who goes from "occasionally late" to "consistently later" is showing a change in behavior. That trend can be more meaningful than the absolute number of days past due in a given week.

- 💚 Switching to Autopay. Autopay is a powerful stabilizer. We see a roughly 50% reduction in default when a buyer switches to Autopay. Wholesail also gives you levers to reduce risk, not just predict it.

The score draws on cross-vendor trade behavior from the Lighthouse network when available. When there's no data from other vendors, it uses your historical data on that buyer only.

Why trade data beats credit bureaus

Traditional credit bureaus were not designed around trade credit. In fact, bureau reports contain very little information on how wholesale buyers are paying their suppliers. Rather, they primarily reflect how a business is paying its bank products (credit cards, installment loans, lines of credit) — where signs of financial distress typically show up later than they do in supplier payment behavior.

Wholesail's model is trained on trade payment data specifically: invoices, payments, aging, and open balances flowing directly from vendor ERPs across the Wholesail network. Because these integrations update daily, the model is working with current behavior — not a snapshot that might be weeks or months old. See our full list of integrations.

That makes it purpose-built to answer the question vendors actually care about: how likely is this buyer to pay?

How teams use Risk of Default Scores

Think of the score as a meaningful edge. We've quantitatively demonstrated that a customer with a higher Risk of Default score is more likely to actually default than a customer with a lower score 72% of the time. That's substantially better than random chance or aging alone. If you act on risk scores consistently across your customer base, you'll come out ahead over time by catching more problems early and extending terms where it's warranted.

Any individual score reflects probability, not certainty — so treat it as one input alongside your knowledge of the customer.

#1 · Prioritize collections efforts by probability of loss

Unlike Aging (which just shows who is late), the Risk of Default score tells you who is most likely not to pay.

- A customer who is 45 days late but scored 🟢 Very low risk may be a habitual slow payer who always eventually pays; they need consistent follow-up, but they're unlikely to become a loss.

- A customer who is only 10 days late but scored 🟠 High or 🔴 Critical risk may be showing early signs of cash flow trouble and deserves earlier, more urgent outreach before their balance grows further.

How to do this in Wholesail

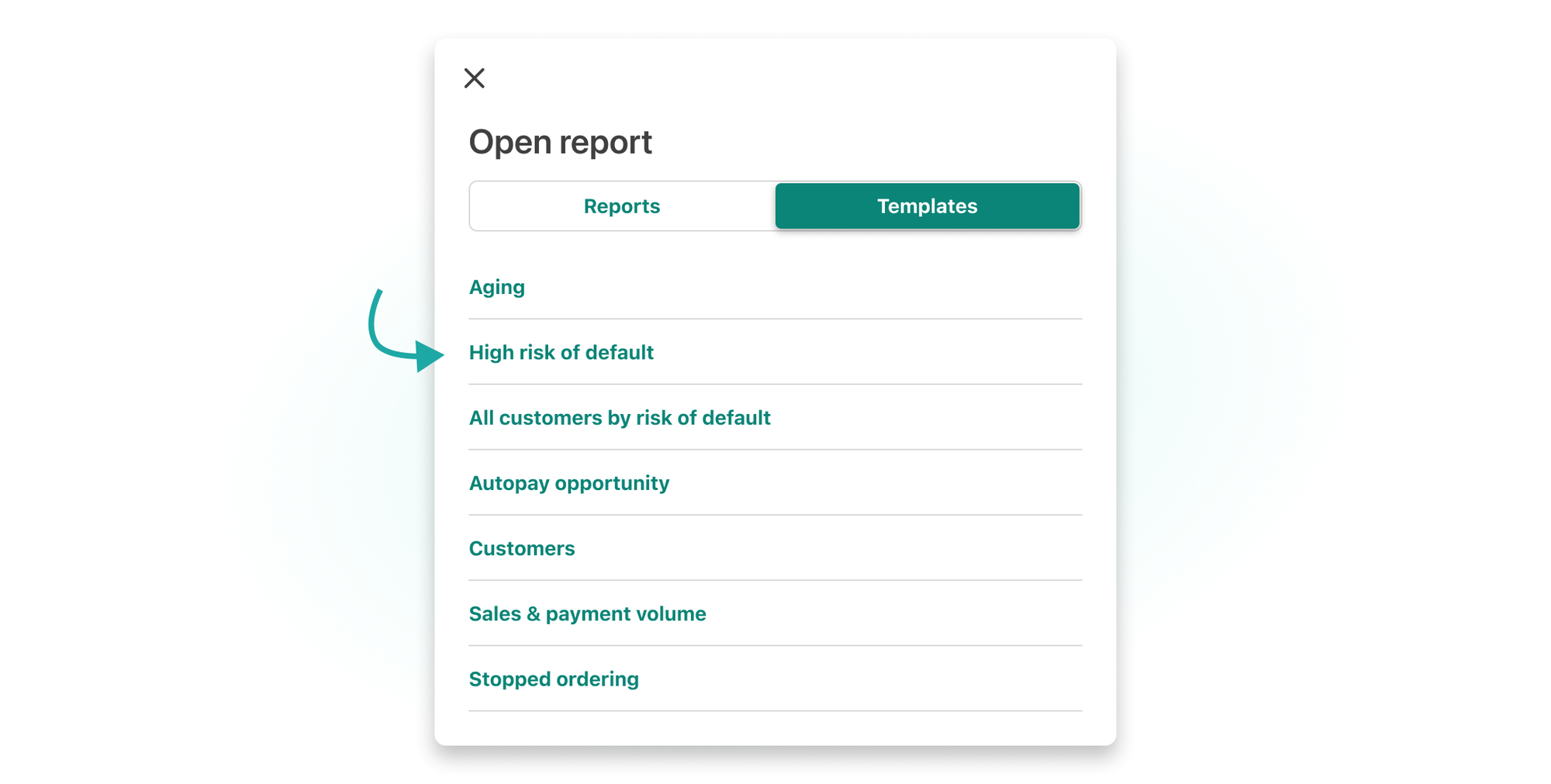

From the customer list, click "Open report" → "Templates" → load the "High risk of default" saved report.

This shows customers with High or Critical risk, sorted by outstanding balance, putting your highest-exposure accounts first. It also includes Lighthouse tradeline ratings, past due balances, and recent payment behavior so you can assess each account in context.

These are accounts where early action — a phone call, a payment plan conversation, a request to set up Autopay — is most likely to prevent a loss.

One of our customers recently shared “If I’d seen that earlier, I never would have let my exposure get as high as it did. With that visibility upfront, we would have stopped extending credit much earlier.” Read the case study.

#2 · Extend better terms to your best customers

Wholesail's survey found that 70% of buyers would shift weekly purchasing toward a vendor offering better terms. But most vendors don't have a reliable way to know which customers actually deserve them.

The Risk of Default score gives you that lens. A customer who's been on Net-7 for months and consistently scores Very low risk is probably being under-served. Offering Net-14 or Net-21 to a buyer like that encourages larger orders and builds a relationship that's harder for competitors to displace.

On the flip side, a customer who was low risk when you extended Net-30 might now be trending toward Medium or High. That's a signal to tighten terms, lower a credit limit, or require Autopay before the situation deteriorates.

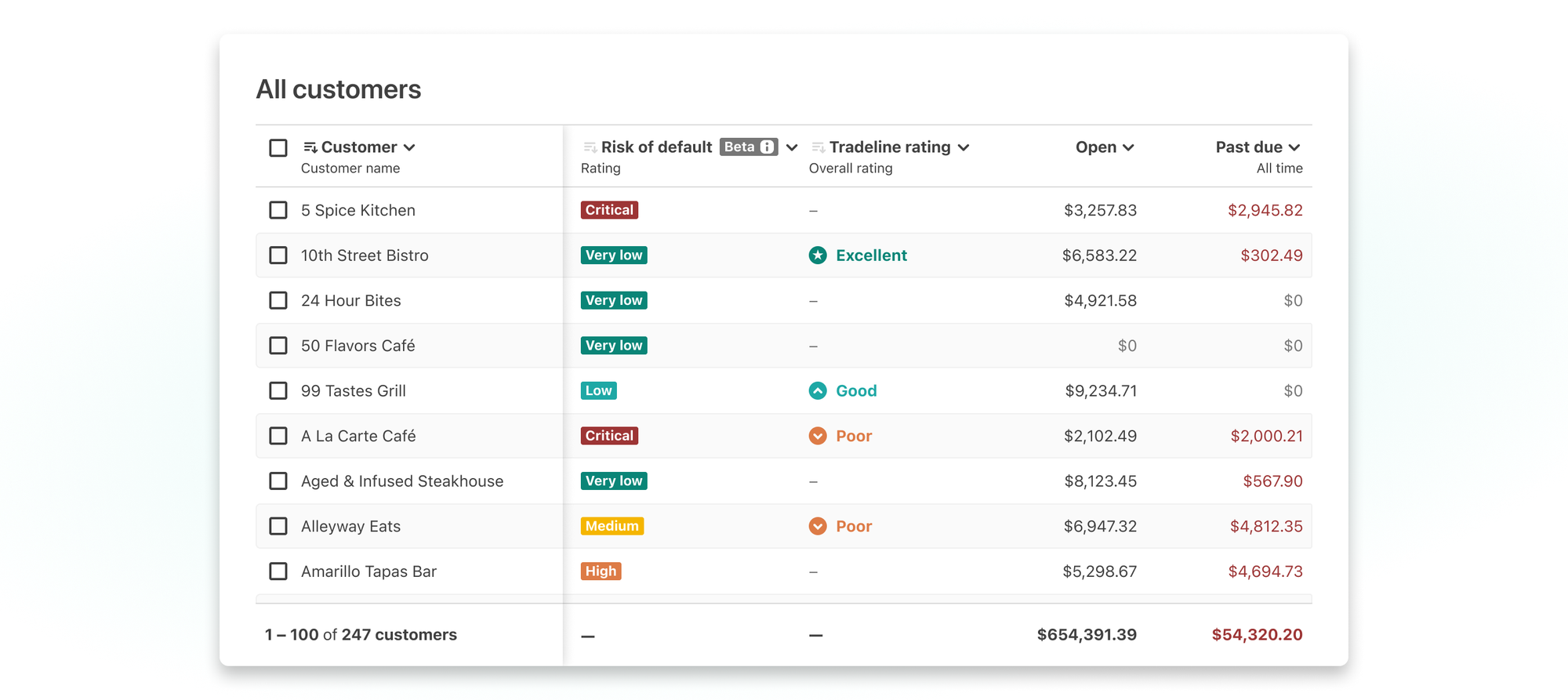

How to do this in Wholesail: Open the "All customers by risk of default" report template to see your entire portfolio sorted by risk, alongside columns for open balance, past due, and purchase history.

Use this as a starting point for reviewing whether their current payment terms and credit limits still match each customer's risk profile.

Use the score alongside what you already know: how long they've been a customer, what your sales rep says about them, whether they're communicative when late. The score adds data to these conversations.

#3 · Evaluate new customers with network data

When a prospective customer applies through your New Customer Form, the Risk of Default score may appear alongside their Lighthouse tradeline report. Because the customer is new to you, the score relies entirely on payment behavior shared across the Lighthouse network – so it's available where there's sufficient network coverage.

How to do this in Wholesail: When reviewing a New Customer Form, check Lighthouse for the Risk of Default score. Where available, it gives you a data point for initial terms and credit limit decisions that would otherwise depend on a credit bureau not built for wholesale trade.

What's next

Over time, the model will continue to evolve as it learns from more real-time payment data across the network. Predictive power will improve as the dataset grows and patterns become clearer. We'll keep refining how we evaluate performance to ensure the score remains reliable and actionable.

We're also exploring building workflows that connect risk signals directly to the credit and collections decisions your team is already making — so you can move from seeing risk to acting on it without leaving Wholesail.

See Risk of Default Scores in Wholesail

Risk of Default Scores are available now for all your existing customers with sufficient payment history. Just opt in to Lighthouse in your Settings to get started.

If you want to see how it works on your portfolio, or how other teams are using it to reduce losses while supporting growth, schedule a demo with the Wholesail team.

Key points:

- Food and beverage distributors extend credit terms to their buyers without real-time payment data.

- Wholesail introduces Risk of Default Scores in Lighthouse, giving customers a buyer-level probability of default directly inside the platform.

- The score uses trade payment data (invoices, balances, payments, and cross-vendor behavior) to classify customers into five risk levels from Very Low to Critical.

- Unlike aging reports or credit bureaus, the model analyzes behavior trends, such as rising balances, increasing lateness, and Autopay adoption, to detect early default risk.

- Distributors can prioritize collections based on likelihood of non-payment, focusing attention on high-risk accounts before losses occur.

- The score also helps vendors safely extend longer payment terms to low-risk buyers, unlocking larger orders and revenue growth.